“People don’t plan to fail, they fail to plan.”

If you are thinking of sending your children to Public School then after you decide which school is the most suitable, you then need to decide how to finance it.

At this point you’re likely to fall into one of to camps in that you’ll either finance it from your income or you’ve saved in advance to provide sufficient resources.

Here are some examples of ways to plan for education expenses.

Example 1

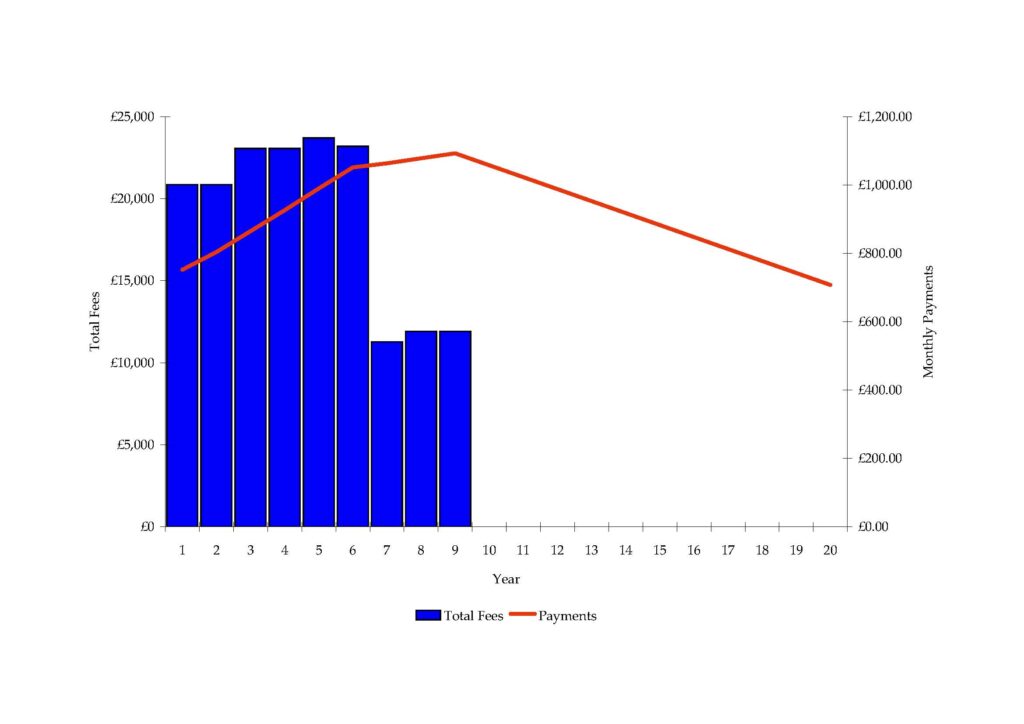

Having just moved to Cardiff because of work, Cerys & David, decide to send their daughters, Emma (year 8) & Jane (year 5) to Howells School Llaandaff. They have no significant savings, but are about to buy a house with the sale proceeds of their previous house.

Rather than buy their house outright they obtain an Offset Mortgage on an “Interest Only” basis which would enable them to pay the fees necessary now and in the future while spreading the repayments evenly over the next twenty years at a cost of £752 per month initially. It will also enable them to have the flexibility to commit additional money to reduce the term.

Example 2

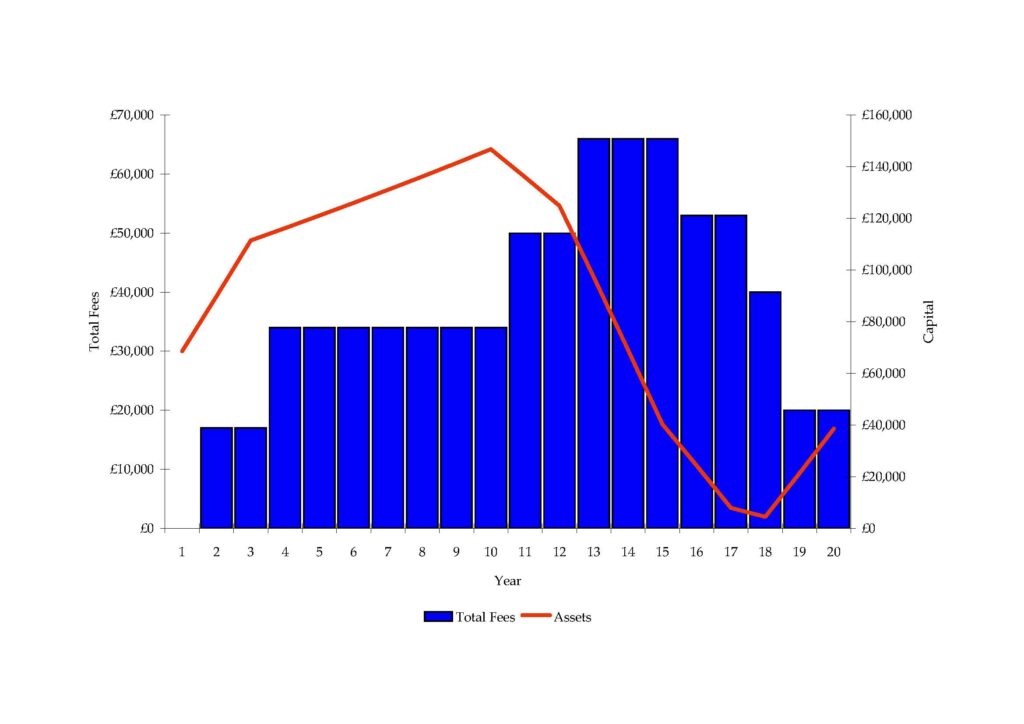

Arabella and James are looking to send their sons, Alex and Ian, to Pilgrims’ School, Winchester College and then onto University. Alex is to start at Pilgrims’ School in a year’s time and they have £50,000 built up already.

We can plan ahead and set up tax efficient savings arrangements to spread the costs so that they simply need to save £3,100 per month throughout the period to cover their School and University costs given the assumptions made.

Example 3

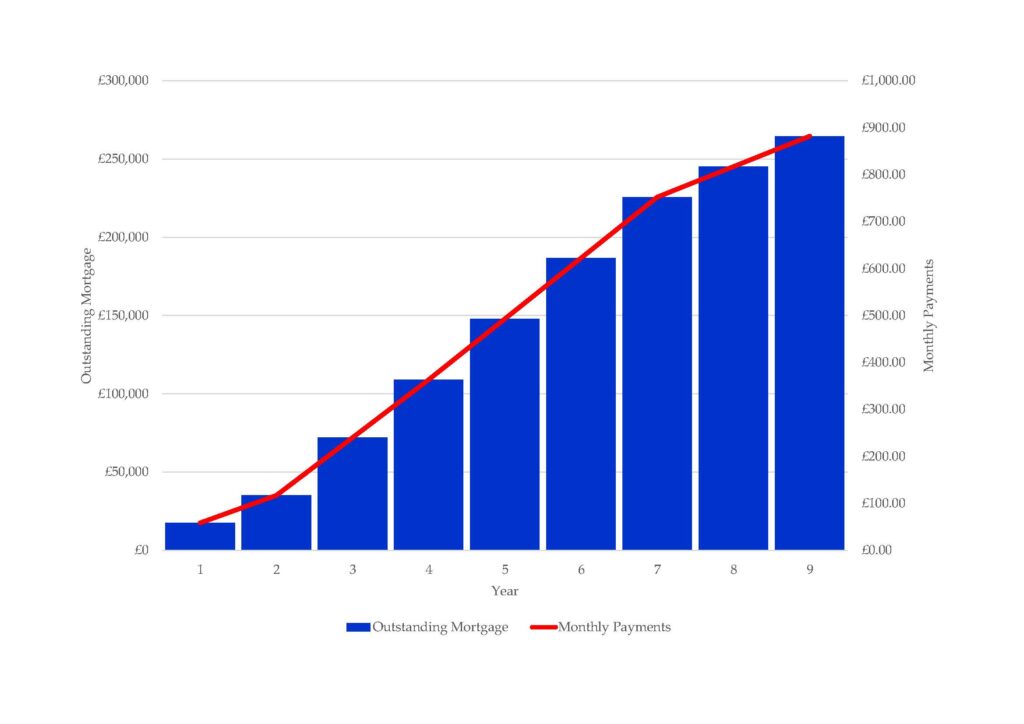

Gillian and Ru are looking to send their children Angelo and Kumar to King’s College School in Wimbledon, they don’t have spare savings, but do have significant equity in their property and excellent pension arrangements thanks to their employers.

By re-mortgaging Gillian and Ru are able access the equity in the property drawing the funds down gradually to pay the School Fees. They are then able to satisfy this extra borrowing using the Pension Commencement Lump Sum from their pensions when they become available.

Example 4

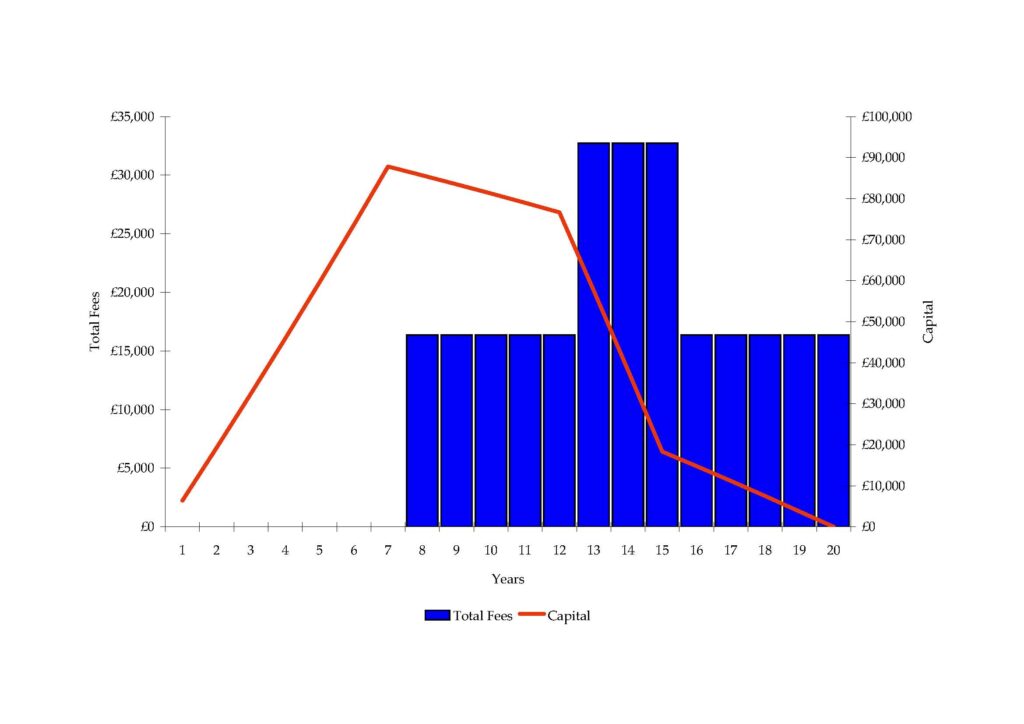

Kate and Steve, while happy with their State Primary School, would like to send their two sons, Tim and Harry, to Whitgift School when they leave. Tim will be going in 8 years and they have no available capital at all currently.

An available option is to construct a plan utilising a portfolio of EISs, VCTs and SEISs to enable the claim of 30% tax relief on the savings made. This means that they only have to save £746 per month (£1,066 with tax relief) to cover the costs of sending their children to the Whitgift School.

Once your plan is made it is vital to consider what may go wrong, with this in mind all our plans make provision for death or health problems by using Wills, Insurances and Trust planning to ensure that all likely problems are covered.

This is provided for information purposes only and does not constitute any form of financial or investment advice. We believe the information in this fact sheet to be correct at the time of going to press but we cannot accept any responsibility for any loss to any person as a result of action or refraining from action as a result of any item herein.